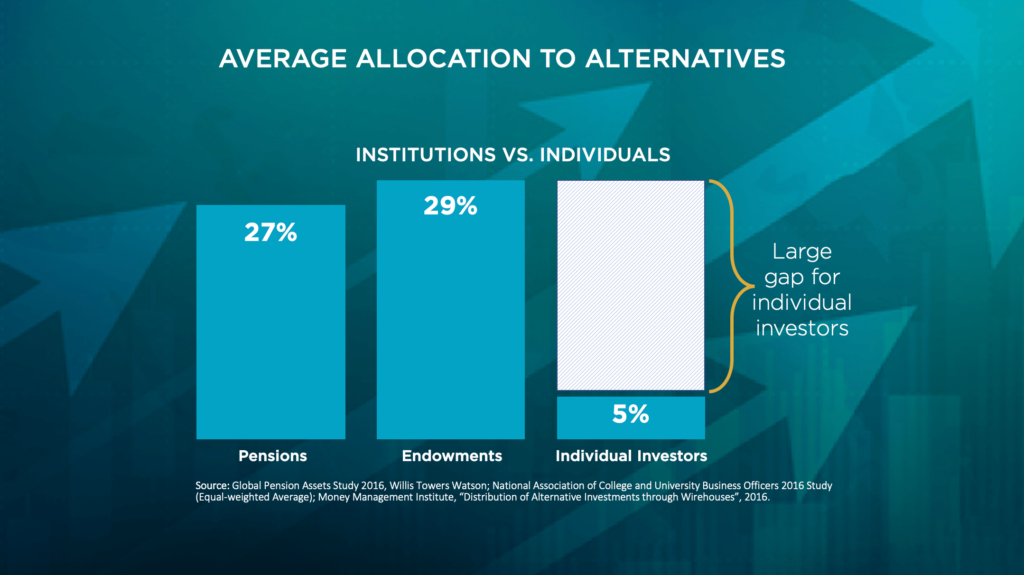

SHOULD YOU INVEST IN ALTERNATIVE INVESTMENTS? Institutions invest far more in alternative investments than individuals do. I put investment advisors into three categories with respect to alternative investments (alts). No Alts – Some advisors stick strictly to...

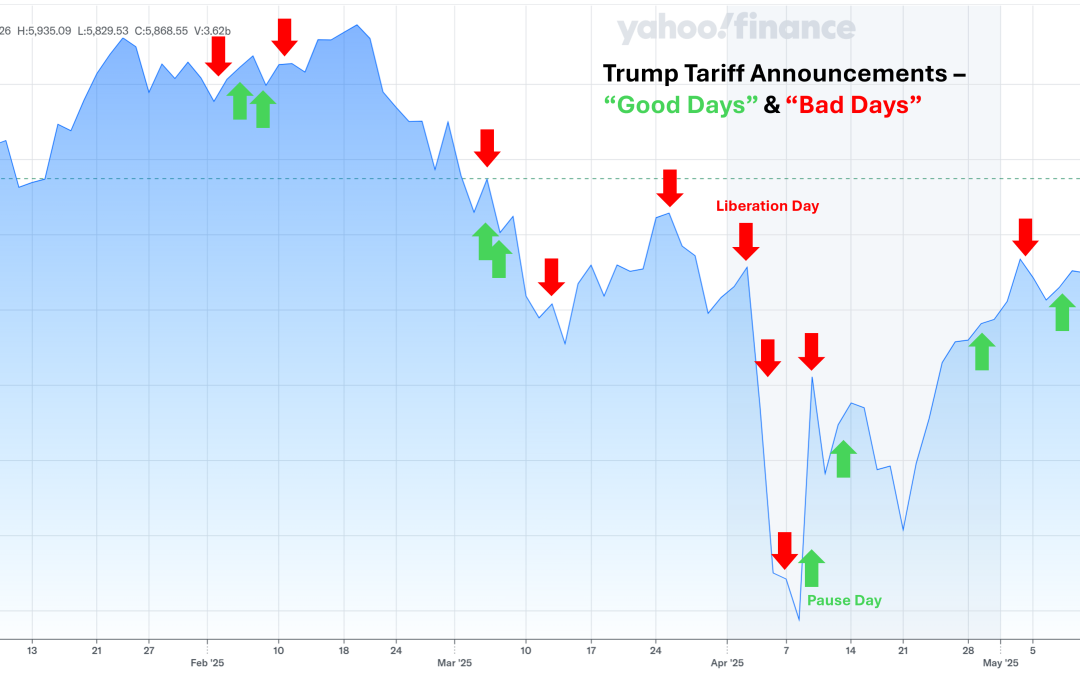

The stock market this year has been fixated on President Trump and his announcements on tariffs. Nothing shows this more plainly than the above chart that demonstrates that stocks have moved almost in lock step with tariff announcements. That’s because...

Trouble in Paradise At the beginning of the year, they stock market was off to a good start, unemployment was low, a new president was in office trying to reduce government waste and overregulation, and the Federal Reserve was lowering interest rates. We saw the...

Providing for your family – Before I tell you why you need a will, let me interject that probably the worst financial outcome when a person dies, is to have a person with minor children fail to purchase life insurance in an amount that along with their other financial...

Whether value or growth investing is the route to better client returns is an often-debated topic. I was recently part of a team that interviewed investment advisors. Like many advisors, especially those who rely heavily on long-term studies and/or who come from an...

Let’s talk about flying through stock market turbulence. I frequently have clients that make decisions about stocks based on the wrong criteria. Now, these things matter deeply to them and usually have to do with their outlook on the future of our country....